Uphold Review: Fees, Safety, and Is It Legit?

Multi-asset trading platforms that let users move between crypto, fiat, and other asset classes from a single account have become a fixture of the US retail market, alongside single-purpose crypto exchanges regulated primarily as money services businesses. Uphold positions itself in that multi-asset category, and its mix of broad asset support, publicized reserve reporting, and a steady stream of mixed customer feedback online makes it a recurring subject of the “is it legit” question that shows up across Reddit threads and app-store reviews. This review looks at what Uphold offers, how its fees and security claims hold up against publicly available documentation, and where the platform tends to draw complaints.

In this article

- At a Glance

- Quick Verdict

- What Is Uphold?

- Is Uphold Safe?

- Uphold Fees Explained

- Uphold Features Beyond Trading

- Uphold Pros and Cons

- Uphold vs Coinbase

- Uphold vs Other Competitors

- Customer Complaints Deep-Dive: Why Can’t I Withdraw My Money From Uphold?

- What Are the Risks of Using Uphold?

- How Trustworthy Is Uphold?

- Getting Started With Uphold

- Frequently Asked Questions

At a Glance

| Founded / HQ | Uphold describes its founding and headquarters details on its own about page; confirm current corporate details there rather than relying on secondary sources.[1] |

| Claimed user base | Uphold’s marketing has referenced a large global user count (in the multi-million range); check the current figure directly on Uphold’s about page.[1] |

| Assets supported | Uphold’s pricing page lists a broad roster of cryptocurrencies alongside fiat currencies and precious metals; the exact count changes over time, so verify it before trading.[2] |

| Fee structure | Percentage-based spreads that vary by asset class, per Uphold’s own fee documentation (see fee table below).[3] |

| Regulatory registrations | Uphold entities have historically registered as a Money Services Business with FinCEN in the US and held cryptoasset registrations in the UK and EU; confirm current standing directly with each regulator’s public register.[4] |

| US state availability | Availability varies by state and can change; check Uphold’s support article on state restrictions before signing up.[5] |

| Cash insurance | Uphold’s terms reference FDIC pass-through insurance on qualifying USD cash balances held at partner banks, subject to standard FDIC limits and conditions; review Uphold’s terms of service and FDIC.gov for the scope of this coverage.[6] |

| Third-party review scores | Trustpilot and app-store ratings fluctuate; check current scores directly rather than relying on a snapshot figure.[7] |

Quick Verdict

Uphold tends to suit users who want a single account for buying and swapping across crypto, several fiat currencies, and precious metals, and who are comfortable with a fee structure built into the bid/ask spread rather than a flat commission. It may also appeal to people interested in Uphold’s staking program for eligible assets. Active traders who need deep order books, advanced charting, or fast phone-based support may find better alignment with a pure-play exchange. Overall, Uphold appears to be an operating, registered platform rather than an outright fraud, but prospective users should weigh its cost structure and the pattern of withdrawal-related complaints discussed later in this review before funding an account.

What Is Uphold?

Uphold markets itself as a “universal” account that lets users hold and exchange dozens of cryptocurrencies, multiple fiat currencies, and precious metals from one balance, rather than requiring separate accounts or wallets for each asset class. The company’s own about page is the authoritative source for its founding history, corporate structure, and headquarters location, and readers should consult it directly for current details rather than assuming information from older secondary coverage.[1]

Uphold operates through more than one corporate entity depending on jurisdiction, commonly referenced as a US entity subject to FinCEN money-services-business rules, alongside a European entity that has held cryptoasset registrations with UK and EU regulators. These registrations are not the same as full banking or investment-firm licenses; they typically mean the entity is registered for anti-money-laundering supervision rather than prudentially regulated in the way a bank or broker-dealer is. Readers can confirm current registration status through FinCEN’s registrant search, the UK FCA’s public register, and Lithuania’s FCIS/FNTT register, since Uphold’s European operations have referenced Lithuanian licensing in some markets.[4][8][9]

The core differentiator versus a conventional crypto exchange is the “anything-to-anything” trade model: rather than routing every trade through a base currency order book, Uphold prices direct conversions between asset pairs (for example, a cryptocurrency directly into a foreign fiat currency or into a precious metal position) using its own internal pricing engine.

Is Uphold Safe?

Safety on a custodial platform breaks down into a few separate questions: does the platform hold customer assets responsibly, is it subject to meaningful regulatory oversight, and has it experienced security incidents or enforcement actions. Each deserves its own look.

Custody and Reserve Reporting

Uphold publishes a transparency page describing its reserve reporting practices, which the company has described as showing asset holdings against customer balances on a recurring basis. Because reserve-reporting methodologies and update frequency can change, readers should review Uphold’s transparency page directly rather than relying on older descriptions of the feature.[10] This kind of public reserve attestation is broadly similar in spirit to proof-of-reserves initiatives that other large exchanges, including Coinbase and Kraken, have published in various forms, though methodologies differ across platforms and none of these disclosures function as a full independent financial audit in the way that term is used for regulated banks.

Account Security Features

Uphold’s account-level protections typically include two-factor authentication, biometric login on its mobile app, and options for withdrawal address management. Specific configuration details and any recent security-feature changes are best confirmed in Uphold’s own support documentation before relying on them for account setup.

Insurance Coverage

Uphold’s terms of service reference FDIC pass-through insurance applying to qualifying USD cash balances held at partner banks, a structure common among fintech platforms that park customer cash with FDIC-member banks. This type of coverage protects against the failure of the partner bank holding the cash; it does not protect against the loss in value of cryptocurrency holdings, which are not deposit accounts and are not FDIC-insured under any circumstance. The exact dollar limit Uphold references, and the precise conditions under which pass-through coverage applies, should be confirmed in Uphold’s current terms of service and cross-checked against FDIC.gov’s general guidance on pass-through insurance.[6]

Regulatory Standing and Past Actions

In April 2026, the New York Attorney General announced a $5 million settlement with Uphold over its role in promoting CredEarn, a cryptocurrency lending product operated by the now-bankrupt Cred LLC, between January 2019 and October 2020. The state alleged Uphold marketed CredEarn as safe and insured while the underlying lending activity carried undisclosed risk; Uphold did not admit liability and has said it was itself misled by Cred, and settlement funds are earmarked for affected customers. Beyond that settlement, no specific NYDFS enforcement action or SEC action naming Uphold could be confirmed from the sources reviewed. That is not a guarantee that none exists or that none will occur; readers who want a current, authoritative answer should search NYDFS’s enforcement actions database and SEC’s EDGAR and litigation-release systems directly, and review the Attorney General’s published settlement announcement for details on the CredEarn matter.[11][12][17]

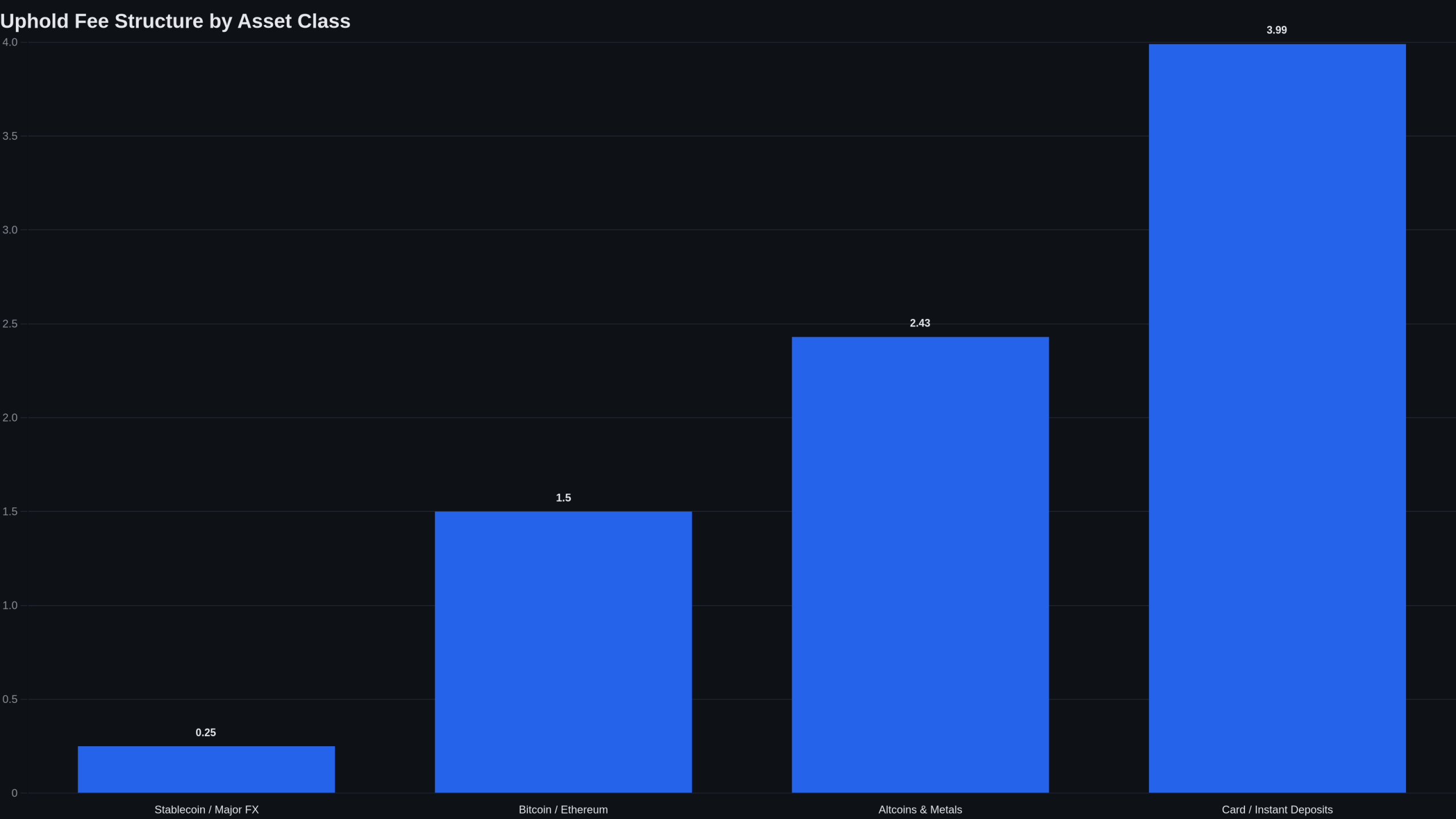

Uphold Fees Explained

Uphold does not charge a simple flat percentage on every trade. Instead, its published fee documentation describes variable spreads that differ by asset class, generally lower for stablecoin and major-fiat conversions, and higher for less liquid cryptocurrencies and precious metals. Because these figures are set by Uphold and can change without much notice, treat the ranges below as directional rather than exact, and confirm the current schedule on Uphold’s own fee support page before trading.[3]

| Fee type | What Uphold’s documentation describes |

|---|---|

| Stablecoin / major FX pairs | Historically described as the lowest spread tier on the platform |

| Bitcoin / Ethereum | A moderate spread tier, higher than stablecoin pairs |

| Altcoins and precious metals | The highest spread tier, reflecting lower liquidity |

| Card deposits | Card-network processing fees may apply in addition to the trading spread |

| USD wire withdrawal | Historically free for wires of $2,000 or more; a $10 fee has historically applied below that threshold. Confirm the current amount before initiating a wire |

| Crypto network withdrawal | A flat $0.99 fee has historically applied to most crypto network withdrawals (Bitcoin, XRP, and HBAR networks are excluded from this flat fee), on top of network/miner fees that are passed through and vary with blockchain congestion |

| Monthly / inactivity fee | Uphold has not historically charged a monthly or inactivity fee; confirm current policy directly with Uphold support, as fee policies of this kind can change |

Fees and availability verified as of July 4, 2026.

Because Uphold’s cost is embedded in the spread rather than displayed as a separate line-item commission, the effective cost of a trade is easy to underestimate. On a hypothetical $500 purchase of bitcoin, for example, the quoted price already includes Uphold’s markup, so the amount of bitcoin credited to the account may be measurably less than what a $500 purchase would yield on a platform charging a lower, clearly disclosed maker/taker fee. Readers comparing platforms should look at the effective all-in cost of a trade, not just the advertised “fee” percentage, and our guide to crypto exchange fees walks through how spread-based and commission-based pricing compare across different platforms.

How Uphold’s Fees Compare

Coinbase and Kraken publish their own maker/taker fee schedules, which are structured differently from Uphold’s spread model and change periodically based on tier and volume. Rather than restate specific percentages that could be out of date by the time this article is read, we recommend checking each platform’s current schedule directly: Coinbase’s advanced fee page and Kraken’s fee schedule page are the authoritative sources.[13][14] As a general pattern, spread-based multi-asset platforms like Uphold tend to run more expensive for large single-asset crypto trades than dedicated exchanges with tiered maker/taker pricing, particularly for high-volume traders. For a broader comparison of platforms by cost and feature set, see our best crypto exchanges roundup.

Uphold Features Beyond Trading

- Anything-to-anything swaps: direct conversion between crypto, fiat, and metals without routing through a single base currency.

- Staking: Uphold offers staking rewards on select proof-of-stake assets; advertised annual percentage yields vary by coin and by market conditions, so check Uphold’s earn page for current rates rather than a fixed number.[15]

- Vault: a separate holding area some users describe as intended for longer-term storage outside the main trading balance.

- Recurring buys: scheduled purchases at set intervals for users practicing dollar-cost averaging.

- Crypto baskets: pre-built groupings of multiple assets intended to simplify diversification for less active users.

- Uphold Card and rewards: a debit card product tied to the account balance, with a rewards structure that has evolved over time, check current card terms before applying.

Uphold Pros and Cons

Pros

- Broad multi-asset access from a single account, spanning crypto, multiple fiat currencies, and precious metals.

- Publicly stated reserve-reporting practices intended to give users visibility into how customer assets are backed.

- Staking available on a range of proof-of-stake assets without needing a separate staking wallet.

- FDIC pass-through insurance referenced for qualifying USD cash balances (subject to standard limits and conditions).

- Simple, beginner-oriented interface for cross-asset conversions.

Cons

- Spread-based pricing can be more expensive than commission-based exchanges for large or frequent crypto trades.

- Limited advanced trading tools compared with dedicated crypto exchanges (basic charting, fewer order types for active traders).

- Customer support is reported by some users as slow, with no widely advertised live phone line.

- A recurring pattern of online complaints about withdrawal delays tied to account verification holds (detailed below).

- State availability and product access can vary and change, requiring users to check current terms.

Uphold vs Coinbase

| Category | Uphold | Coinbase |

|---|---|---|

| Pricing model | Spread built into asset price, varies by class | Published maker/taker schedule (confirm current tiers on Coinbase’s fee page) |

| Asset classes | Crypto, fiat currencies, precious metals | Primarily crypto, with additional products in some regions |

| Staking | Available on select proof-of-stake assets | Available on select assets, with its own fee/reward structure |

| Reserve reporting | Publishes a transparency page describing its reserve practices | Has published its own reserve/asset disclosures in various forms |

| Support channels | Primarily ticket/chat-based support per current documentation | Tiered support depending on account level; confirm current channels |

| Best for | Users wanting one account across multiple asset types | Users prioritizing a large, liquid crypto-focused order book |

Neither platform’s current corporate listing status is asserted here; readers who need that information should consult each company’s investor-relations page or SEC filings directly rather than relying on assumptions about private or public status.

Uphold vs Other Competitors

| Category | Uphold | Kraken | Binance.US |

|---|---|---|---|

| Core model | Multi-asset “anything-to-anything” account | Crypto-focused exchange with margin/futures in some jurisdictions | Crypto-focused spot exchange |

| Fee structure | Variable spread by asset class | Published maker/taker schedule (see Kraken’s fee page) | Published maker/taker schedule (confirm current version directly) |

| Unique differentiator | Fiat currencies and metals alongside crypto | Longstanding advanced trading and margin tools | US-focused spot trading with a narrower asset list historically |

For a deeper side-by-side breakdown of individual exchanges, see our related comparisons, including Kraken Review, Coinbase vs Kraken, and Binance vs Kraken.

Customer Complaints Deep-Dive: Why Can’t I Withdraw My Money From Uphold?

A recurring theme across Reddit’s r/uphold community and app-store reviews involves users reporting that withdrawals were delayed or blocked after they attempted to move funds off the platform. Several posts describe this happening around the time of a large deposit or withdrawal, or after a period of account dormancy.[16]

Financial platforms subject to anti-money-laundering rules are generally required to conduct enhanced verification or compliance review when account activity looks unusual relative to a user’s normal pattern, for example, a sudden large deposit followed by an immediate withdrawal request, or renewed activity on a long-dormant account. This kind of hold is a common industry practice across regulated money-services businesses, not unique to Uphold, though it is understandably frustrating for the user experiencing it, and delays can stretch on longer than users expect if documentation requests aren’t resolved quickly.

It is worth noting the gap between Uphold’s aggregate review scores on sites like Trustpilot, which have historically skewed positive, and the more negative tone found in Reddit threads and app-store comment sections.[7] This divergence is a known pattern across many consumer platforms: dissatisfied users are more likely to post detailed complaints on open forums, while satisfied users are less likely to leave a review at all, which can skew forum sentiment more negative than a platform’s typical user experience.

For users experiencing a withdrawal delay, a documented escalation path generally works better than repeated support tickets alone: gather account verification documents in advance, respond promptly and completely to any compliance request, and if the issue remains unresolved after a reasonable period, consider filing a complaint with the Consumer Financial Protection Bureau or the relevant state financial regulator, which creates a formal record and can prompt a platform response.

What Are the Risks of Using Uphold?

Beyond the withdrawal-hold pattern described above, a few broader risk categories apply to any custodial multi-asset platform, including Uphold:

- Custodial risk: assets held on Uphold are not self-custodied. Users do not control private keys, meaning platform-level issues (technical, operational, or regulatory) could affect access to funds, the standard “not your keys, not your coins” caveat applies here as it does to any custodial exchange.

- Fee drag: spread-based pricing can meaningfully erode returns for frequent traders compared with commission-based platforms, especially on less liquid assets.

- Regulatory complexity: operating across multiple jurisdictions under different registration regimes (FinCEN in the US, cryptoasset registrations in the UK and EU) means the applicable consumer protections can differ by region and may not match the protections of a fully licensed bank or broker-dealer.

- Support responsiveness: as noted, resolving account or verification issues may take longer than users expect, which is itself an operational risk worth weighing before depositing large sums.

How Trustworthy Is Uphold?

Weighing the available evidence: Uphold operates a real, functioning platform with public transparency reporting, cross-jurisdiction regulatory registrations, and a fee structure disclosed (if not always intuitively) in its own support documentation. That combination is generally consistent with a legitimate, if imperfect, regulated fintech operator rather than an outright fraudulent scheme. At the same time, the volume and consistency of withdrawal-delay complaints across independent forums suggests real friction in Uphold’s compliance-review and customer-support processes, friction that can feel indistinguishable from fraud to an affected user, even when it stems from standard AML procedures rather than bad-faith fund retention. Uphold’s 2026 settlement with the New York Attorney General over its promotion of the third-party CredEarn lending product is a separate, material trust data point: it shows real regulatory consequences tied to past marketing practices, even though the underlying fraud was committed by a lending partner rather than Uphold itself, and even though Uphold has since paid to help make affected customers whole. The most balanced reading is that Uphold is a regulated, operating platform with a documented past-marketing settlement and genuine customer-service and scaling gaps, not a platform built to withhold funds as a matter of policy, though individual users should still weigh their own risk tolerance and documentation habits before depositing significant sums.

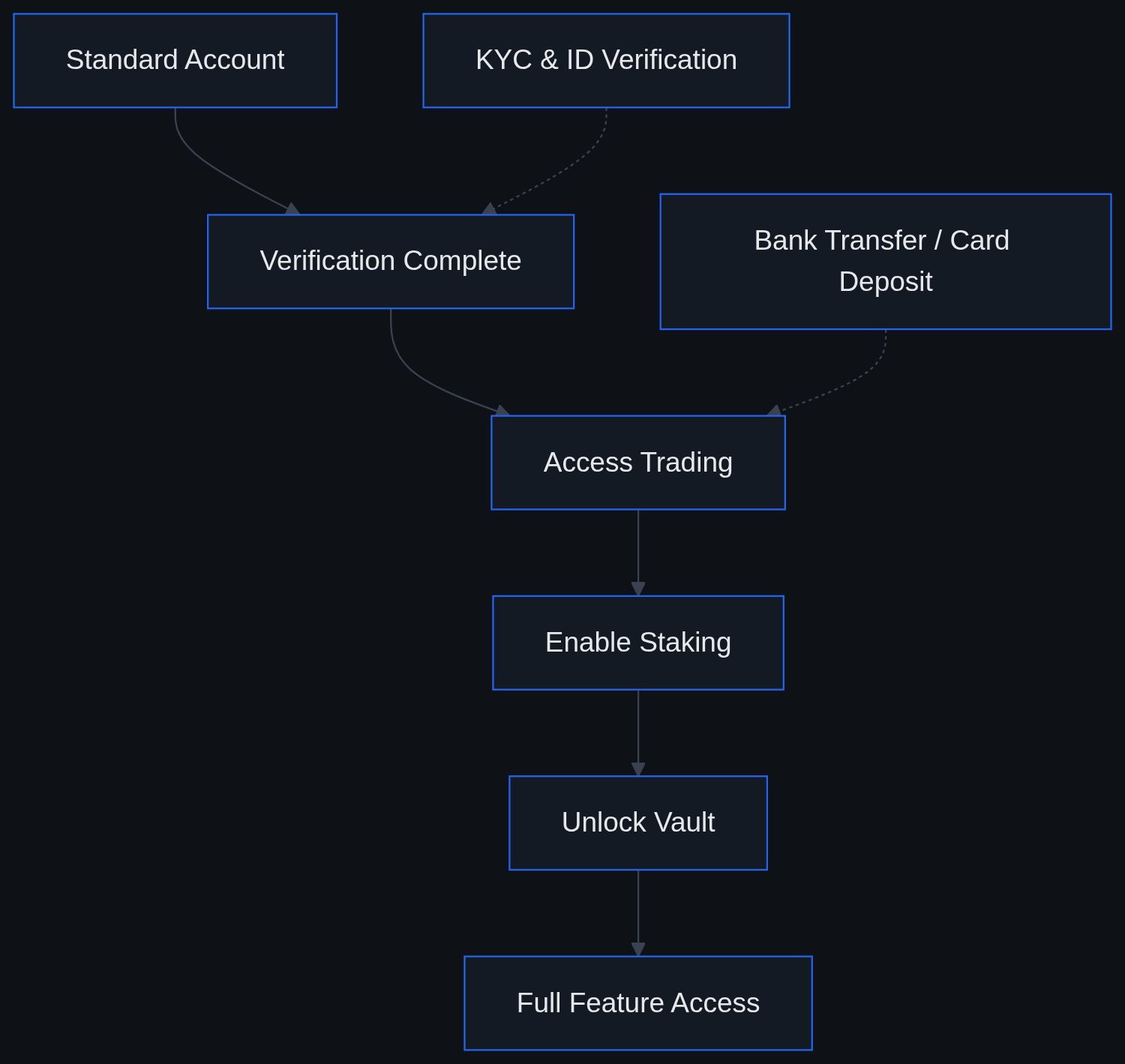

Getting Started With Uphold

- Create an account and complete identity verification (KYC), which typically requires a government ID and basic personal information.

- Fund the account via a supported method, bank transfer, card, or crypto deposit, checking current processing times and fees for each method first.

- Decide whether to hold assets in the main trading balance or move eligible holdings into Uphold’s Vault feature for longer-term storage.

- Set up staking on eligible assets or configure a recurring buy schedule if pursuing a dollar-cost-averaging approach.

Common pitfalls include underestimating the spread cost on less liquid assets, assuming a flat fee applies uniformly across all trades, and not budgeting extra time for identity verification if a large deposit or withdrawal triggers a compliance review.

Frequently Asked Questions

Is Uphold legit or a scam?

Available evidence points to Uphold being an operating, registered platform rather than a fraudulent scheme, though it carries a documented pattern of user complaints about withdrawal delays and a 2026 New York Attorney General settlement over its promotion of a third-party crypto lending product. Confirm current regulatory registrations directly through FinCEN’s and the FCA’s public registers before depositing funds.

How trustworthy is Uphold?

Uphold publishes reserve-reporting information and maintains multi-jurisdiction regulatory registrations, which support a baseline case for legitimacy. Its fee structure, a recurring pattern of support-related complaints, and a 2026 $5 million New York Attorney General settlement over its promotion of a third-party crypto lending product are the main factors weighing against a stronger trust rating; the settlement involved a lending partner’s product rather than direct fraud by Uphold, but it remains a material regulatory data point.

Why can’t I withdraw my money from Uphold?

The most commonly cited reasons in user reports involve compliance or verification holds triggered by unusual account activity, such as a large sudden deposit-and-withdrawal pattern or renewed activity on a dormant account. These holds are standard practice at regulated money-services businesses, though resolution times reported by users vary.

What are the risks of using Uphold?

Key risks include custodial risk (Uphold, not the user, controls the underlying keys), fee drag from spread-based pricing on frequent trades, multi-jurisdiction regulatory complexity, and potential delays in customer support resolving account issues.

Does Uphold have a monthly fee?

Uphold has not historically charged a monthly or inactivity fee. Its official fee support documentation sets out current policy and can change, so check that page directly before relying on any older description of the fee structure.

Is Uphold better than Coinbase for beginners?

It depends on what a beginner values most. Uphold’s appeal is a single account spanning crypto, fiat currencies, and metals, which may suit users who want simplicity across asset types. Coinbase’s appeal for many beginners is a large, liquid crypto-focused marketplace with a more conventional fee schedule. Reviewing both platforms’ current fee pages and our best crypto exchange for beginners guide can help clarify which fits a given use case.